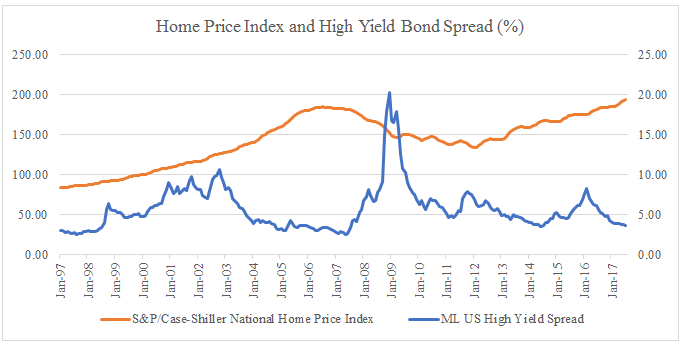

The bull market is in a full swing and everything is becoming more and more expensive. The US equity markets are hitting record highs day after day. The cyclically-adjusted PE ratio (Shiller PE) has reached 31.2, which is 90% higher than its historical average of 16.8 since 1880 (see Figure 1). High yield bonds, the fixed income instruments with the lowest credit qualities, joined the rallies as well. The credit spread of the high yield bonds has declined to 370 basis points, which is well below its historical average of 573 basis points since 1997. Housing prices nationwide have recovered and exceed the pre-crisis levels (see Figure 2).

Figure 1. Shiller PE

Source: Multpl.com

Figure 2: Home Price and High Yield Bond Spread

Source: FactSet.

Astonishingly, synthetic CDOs, which rose to notoriety during the subprime crisis and then faded into obscurity after nearly destroying the financial system, staged a comeback. Banks have issued roughly $70 billion of synthetic CDOs in recent years. More ironically, Citi Group, which was bailed out by the government during the financial crisis, emerged as a dominant player in the market. The high valuation across the all asset classes and re-emergence of complex financial instruments make investors wonder: are we entering another credit-fueled bubble?

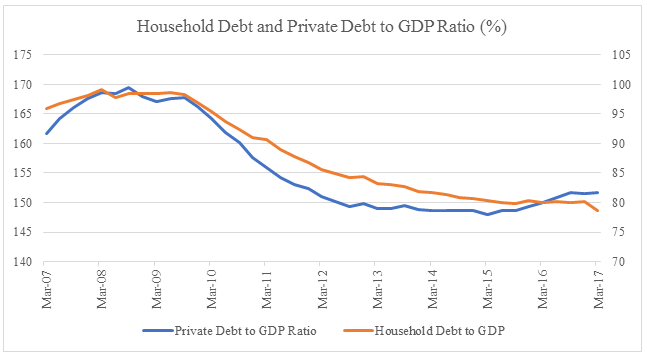

The root cause of the financial crisis was easy credit. Because mortgage loans could be easily repackaged into CDOs, lenders were incentivized to loosen lending standards and underwrite risky loans like subprime mortgages. Meanwhile, homeowners were also incentivized to borrow beyond their means. When the housing market finally collapsed in 2007, mortgage and CDO defaults skyrocketed, resulting in a nationwide financial crisis. After the crisis, despite the extraordinarily low interest rates, the private sectors and households were focusing on deleveraging their balance sheets, and banks were tightening their leading standards under new regulations. Consequently, we have not seen any excessive lending and borrowing for now. Figure 3 shows the private sector and household debts as a percentage of GDP have been declining after they peaked in 2008. The current debt levels are significantly lower. It will be hard to argue that the current high asset valuation is a result of excess credit creation.

Figure 3: Household Debt to GDP and Private Debt to GDP Ratios

Source: FactSet, BIS

In fact, the low interest rates, rather than easy credit, are to be blamed for most of the elevated asset valuation. During the financial crisis between 2007 and 2008, the Fed cut the short-term interest rates from 5% to 0% and kept them close to zero for over seven years until the end 2015. After three rounds of quantitative easing, long-term interest rates were also depressed (see Figure 4). Current short-term interest rates are close to 1% and long-term interest rates are around 2.5%. In this low rate environment, investors have been buying risky assets such as equities, high yield bonds or real estate to seek better returns. Hence, all the assets are becoming more expensive.

Figure 4: Interest Rates

Source: FactSet

The current valuation may not be in bubble territory yet. During the peak of the tech bubble in 2000, the Shiller PE was close to 45, and in the high of the housing bubble, the high yield spread was 257 basis points. However, we may be getting closer to an interest rate driven asset bubble and investors must be cautious. As the Fed continues its path of raising interest rates and unwinding quantitative easing, the high valuation will post an additional risk to an investor’s portfolio. Although valuation may not be a good timing indicator, high valuation will make the market downturn more severe if and when it happens.

__________________________________________________________________________________________

Disclosure

This article is for the purpose of information exchange only. It is not a solicitation or offer to buy or sell any security. You must do your own due diligence and consult a professional investment advisor before making any investment decisions. All information posted is believed to come from reliable sources. We do not warrant the accuracy or completeness of information made available and therefore will not be liable for any losses incurred.