Last week, the stock markets bounced back amid the strong retail sales and upbeat earnings report from Citi Group and Yahoo. S&P 500 Index rallied 2.7% and has recovered most of losses in April. U.S. retail sales recorded their largest gain in one and half years in March at 1.1%, generating optimism that growth may accelerate in the second quarter. Citi Group reported $1.23 EPS, beating estimate of $1.14 EPS. Yahoo met expectation with 1% rise in revenue, showing an encouraging sign of growth.

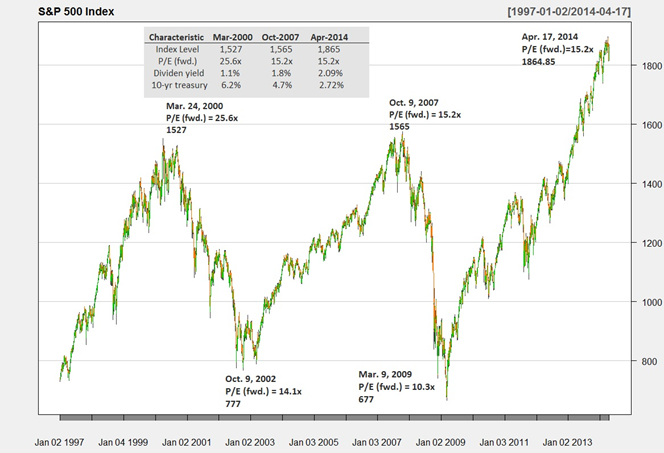

Despite the last week’s good news and our bullish views on stocks (see our last week’s report “Crash in 2014, Not So Fast” and stock market trend chart), we are cautious about the US earnings growth. A robust earning growth is achievable if the economy accelerates to support stronger sales growth in the rest of 2014.

{kind=link}

At the beginning of this year analysts estimated double-digit profit for 2014. Consensus bottom-up forecasts expect that earnings generated by S&P 500 companies in 2014 would expand by 10.6% to a record high of nearly $120 per share. For sure, investors have good reason to expect better profit growth in 2014: the U.S economy is strengthening; the economy of Europe is improving. However, when companies started to release their financial results, this estimate seems to be overly optimistic. As of April 17, 2014 the blended earnings growth rate is 1.7% over Q1 2013. Of the 82 companies that have reported earnings 66% have reported actual EPS above the mean EPS estimate. The percentage is below both the 1-year (71%) average and the 4-year (73%) average.

Two main factors are believed to have resulted in the lower earnings in Q1. One factor is the less favorable FX rates. The U.S. dollar has strengthened relative to major currencies over the past year. A number of companies have cited the negative impact of foreign exchange in their earnings releases. The other factor is the slowing emerging market. Growth in emerging markets has been flat or slightly below a year ago. China, especially, has seen significant slowdown in growth. In addition, the extreme weather in Q1 also has negative impact on Q1 earnings – companies have cited this in their earnings releases.

There are a few additional reasons to concern about this year’s earrings. One reason is the peaking profit margin of U.S. companies. S&P 500 companies have become more and more rely on cost cut to fuel profit growth. The profit margin is already at a high level. Without technology innovation it will become harder and harder to increase profit margin.

Source: Standard & Poor’s * S&P 500 operating earnings per share / sales per share

Slower sales growth is another thing to concern about. Real sales growth for S&P 500 companies has decreased over 4% since Q4 2011. As of Q4 2013 this number was as low as 0.75%. To achieve double digit expansion in earnings a higher sales growth is needed.

Source: Standard & Poor’s

To achieve higher sales growth, the economy needs to grow at a faster pace. Can the economy increase earnings? As shown in the following chart, earnings and real GDP tend to grow at similar rates. However, the estimated earnings (green columns) are growing at a much higher rate than the real GDP growth rate in recent years. If the economy can growing at a higher rate this year then higher earnings will be likely.

Although we need to be cautious about those estimates, there are some positive news. The U.S. economy is continuously improving. The Fed is tapering stimulus slower than expected. Hiring and corporate spending is increasing. Rising stock prices and higher home prices have fueled consumer spending and boosted consumer confidence. In Europe, the recession has ended and a recovery is underway – an increase in GDP of 1.1% was recorded in Euro Zone in Q4 2013. The emerging markets, although have experienced slowdown, are still robustly growing. The fact that China is no longer growing at double digit might disappoint some people, but high single digit growth is still attractive. Thus, we still believe that a robust earning growth is achievable given the positive economic tailwinds for the rest of 2014.

Top Economic News to Watch This Week

Monday:

Chicago Fed National Activity Index (Apr)

Tuesday:

Existing Home Sales Change (Mar)

Wednesday:

US New Home Sales (Mar); Bank of England Minutes; China HSBC Manufacturing PMI (Apr)

Thursday:

Initial Jobless Claims (Apr 18); US Durable Goods Orders (Mar); Japan National Consumer Price Index (Mar)

Friday:

Reuters/Michigan Consumer Sentiment Index (Apr)

Major Earnings Release This Week

Monday:

Tuesday:

Wednesday:

Thursday: Microsoft Corporation (MSFT), Starbucks Corporation (SBUX)

Friday: Principal Financial (PFG)