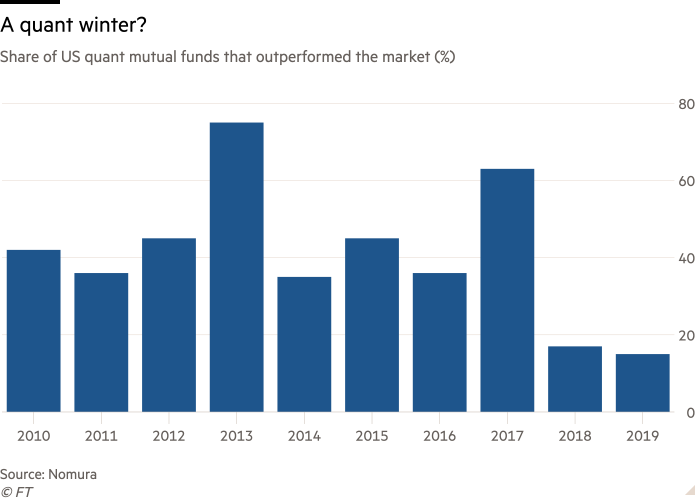

From 2010 to 2017, quant managers generally did a better job than fundamental managers at beating their benchmarks, according to Nomura (see graph below). However, in the last couple of years, quant strategies have been underperforming and experiencing a two-year-long so called “quant winter.”

There are various reasons for the underperformance. Most notably, the correlations between factor performance have been increasing. For example, low valuation and low volatility are tracking each other more closely than ever before. Additionally, interest rates and Fed policies have increasingly become the main performance driver for stock markets, leaving less opportunity for quant managers to distinguish themselves from the crowd.

In this article, we will attempt to explain why quant strategies have periods of over/underperformance using the fundamental law of active management (Grinold, 1989). This law states that:

Where IR is the information ratio, N is the breadth, and E(IC)

is the expected information coefficient (IC). The breadth represents the number of independent investment opportunities in a year. It can be treated as a number of stocks in a selection pool for a quant strategy. An IC is a correlation coefficient between an alpha factor and forward returns of stocks in the selection pool. In this formula, it’s clear that IC is the main driver of over/under performance for a quant strategy.

The IC’s absolute value and variation are used to access its strength; absolute value measures accuracy while variation measures the stability of return forecasts in a selection pool. In this sense, a quant strategy can have strong but volatile returns if it has a high absolute size and a high variation for the IC.

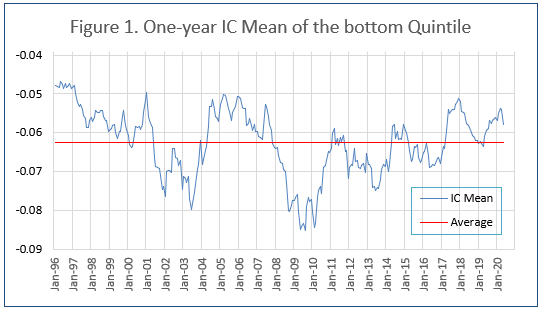

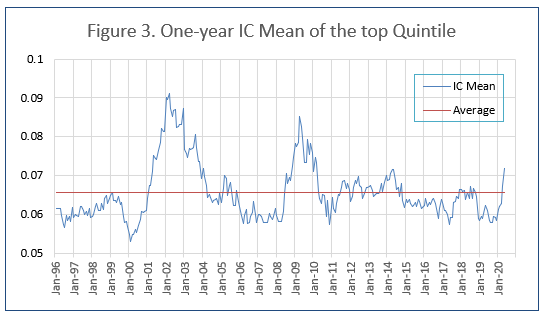

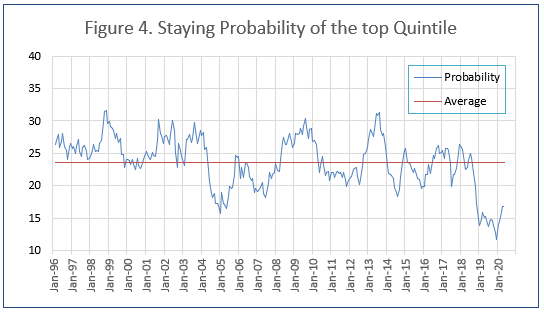

We study quant performance by investigating a group of ICs. First, we divided ICs into quintiles. We assume that quant managers have the skill to choose ICs from the top or bottom of quintiles. Then, we compute the mean of the top (bottom) quintile and probability of ICs staying in the top (bottom) quintile from one period to next period. The means and staying probabilities of the top and bottom quintiles are used to gauge the accuracy and variation of stock return forecasts. Last, we examine quant performance in a sample period.

We calculate ICs using alpha factors from Zeng Systems’ database and stocks from the Russell 1000 index. The database has 251 alpha factors from December 1994 to May 2020. Figure 1 & 3 show the IC mean of the bottom and top quintile, respectively. Figure 2 & 4 demonstrates the staying probability of the bottom and top quintile for the following month, respectively.

Figures 1-4 show that US large cap quant strategies have experinced periods of both strong and weak performance since 1995. For instance,the strategies had great performance from 2002 to 2004 as absolute means and staying probabilities of ICs were high in both the bottom and top quintiles. However, the stategies had poor returns in 2019 due to low absolute means and low staying probabilities of ICs in the bottom and top quintiles. In the past, most quant strategies had better returns when both IC absolute means and staying probabilities are high, though a few quant strategies achieved outstanding returns in a period of low staying probabilities from top and botom quintiles.

The figures also reveal that recent absolute means and staying probabilities of top quintiles are trending up, and staying probabilities of bottom quintiles are moving up. It may indicate that the enviroment is improving for quant investment in US large cap stocks. Quant strategies may be able to perform again in the near future as the improvement continues.

Disclosure: This article is for the purpose of information exchange only. It is not a solicitation or offer to buy or sell any security. You must do your own due diligence and consult a professional investment advisor before making any investment decisions. All information posted is believed to come from reliable sources. We do not warrant the accuracy or completeness of information made available and therefore will not be liable for any losses incurred.