The third quarter was more or less the continuation of the second quarter in terms of economic and market performance. Solid economic growth and strong corporate earnings drove US stocks higher. However, trade tensions and rising interest rates generated significant headwinds. International equities, including both developed markets and emerging markets, underperformed the US equities. EM equities had negative returns in aggregate.

The global economy still grew at a solid pace. The second quarter US GDP grew at a 4.1% annual pace, the highest since 2014. Both Europe and Japan had positive growth rates, 2.0%, and 1.3%, respectively. In the emerging markets, the Chinese GDP growth continued at 6.7% and India’s economy expanded by 8.2% from a year ago, according to FactSet. The world GDP grew 3.1% from a year ago.

Q2 corporate earnings continue to be very strong. Among the companies in the S&P 500 Index, 80% have beaten earnings estimates and 72% have beaten sales estimates. The blended earnings growth rate for the S&P 500 is 25.0%, the highest rate since Q3 2010, according to FactSet.

Monetary policies are tightening, but at a measured pace. The U.S. Federal Reserve raised interest rates on September 26th, lifting the benchmark overnight lending rate by a quarter of a percentage point to a range of 2.00 – 2.25%, as it projected three more years of economic growth in the US. Additionally, the Fed removed the word “accommodative” from its statement, marking the end of loose monetary policies that had been in place since 2008. The central bank still foresees another rate hike in December, and three more in 2019.

Trade tensions between the US and Europe have de-escalated. After meeting with European Commission President Jean-Claude Juncker in July, President Trump said the United States and the European Union would start negotiations immediately on a number of areas that include working toward “zero tariffs” on industrial goods, and further cooperation on energy issues. The two leaders agreed that no new tariffs would be assessed as negotiations proceed.

There was also notable progress on the trade negotiations in North America. The US and Mexico reached a trade deal intending to modernize the NAFTA agreement. Canada was in the process of negotiating with the US to join the revised pact. Mexico has agreed that 75% of its automotive content, up from the current 62.5%, will be produced within the trade bloc (US, Mexico and possibly Canada). Mexico has also agreed that 40 to 45% of the automobile content will be manufactured by workers with a minimum wage of $16 an hour. The agreement also addresses digital data rules that will hopefully better protect intellectual property.

However, the trade war with China has escalated. On September 17th, President Trump announced 10% tariffs on $200 billion worth of Chinese imports, and those duties will rise to 25% at the end of the year. China announced retaliatory measures twenty-four hours later. The Chinese Ministry of Commerce said it would levy tariffs of 5-10% on $60 billion worth of US goods exported to China.

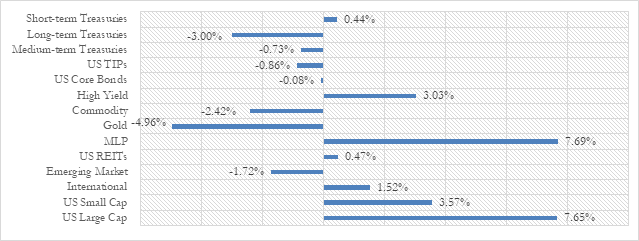

Performance varied widely across asset classes. The S&P 500 Index ETF (SPY) rallied 7.7% and small cap stock ETF (IWM) gained 3.6%. The developed market equity ETF (EFA) rose by 1.5%, but the emerging market equity ETF (VWO) declined by 1.7% as trade tensions hurt the growth prospect in emerging market economies. Gold (GLD) price dropped by 5.0% and Commodity ETF (DJP) lost 2.4%. The energy infrastructure MLPs (AMLP) had another good quarter, up by 7.7% as crude oil continued trading above $70/bbl. With rising interest rates, all the interest rate sensitive assets declined. The long-term Treasury bond ETF (TLT) dropped by 3.0% (see Figure 1). The market volatility, as measured by the S&P 500/CBOE option implied volatility (VIX), declined to a normal level of 12.1% at the end of September.

Figure 1: Asset Class ETF Performance Q3, 2018

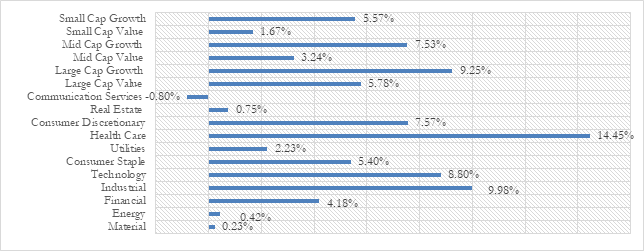

In Q3, large cap stocks outperformed small cap as the trade tensions showed signs of moderation. Most of the sectors generated positive returns. Healthcare sector (XLV) jumped 14.5%, and industrials sector (XLI) was the second-best performer, gaining 10.0%. However, the new communication services sector (XLC) lost 0.8% amid mixed earning results or public backlash against companies like Facebook (see Figure 2).

Figure 2: Equity Sector ETF Returns Q3, 2018

Data Source: FactSet

________________________________________________________________________________________________________

The information in this presentation is for the purpose of information exchange. This is not a solicitation or offer to buy or sell any security. You must do your own due diligence and consult a professional investment advisor before making any investment decisions. The risk of loss in investments can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition.

All information posted is believed to come from reliable sources. We do not warrant the accuracy or completeness of information made available and therefore will not be liable for any losses incurred. No representation or warranty is made to the reasonableness of the assumptions made or that all assumptions used to construct the performance provided have been stated or fully considered.